Lynn C. Klotz, Ph.D. Bridging BioScience & BioBusiness

A small biotech company, virtual or not, has nowhere near $2 billion to bring a drug to market. A simple calculation shows that it can be done for less than $250 million.

In a 2010 study conducted by Eli Lilly and Company, the total cost of drug discovery and development for a single drug was calculated to be about $1.8 billion. The study was based on 2008 data from thirteen large pharmaceutical companies. The cost has increased substantially from $800 million in the late 1990s.

Because of the recent rise of drug development virtual companies, there are a growing number of companies with only one drug candidate in development and none on the market. Virtual companies have no employees except executives, no laboratories, and no manufacturing facilities. They contract out everything from discovery and development through manufacturing. One interesting type of virtual company is formed and funded by patient foundations for so-called orphan diseases, those with less than 200,000 victims.

The cash virtual companies have for drug development may be limited. In any event, a small biotech company, virtual or not, has nowhere near two billion dollars to bring a drug to market. But small biotech companies do bring drugs to market. What is the difference, then, between big pharma and small biotech companies? What is the cost of drug development for these one-drug-candidate biotech companies?

To answer these questions, let’s begin by deconstructing big pharma’s drug discovery and development costs. There are four cost components:

- Discovery

- Preclinical and clinical trials

- Failed drugs

- Cost of capital or time cost of money

The inclusion of research costs for discovery of the drug candidate and of development costs for preclinical and clinical trials are obvious. What may not be so obvious are cost of failed drugs and cost of capital. Since more than eight in nine drugs fail somewhere in clinical trials, the one successful drug must bear the cost of the failed drugs, which can be substantial. Moreover, the pharmaceutical company could have invested the money in financial markets instead of drug discovery and development, so the profit from those alternative potential investments must be accounted for as well. Accounting for this forgone investment profit is called the cost of capital, time cost of money or opportunity cost, and is a legitimate drug discovery and development cost.

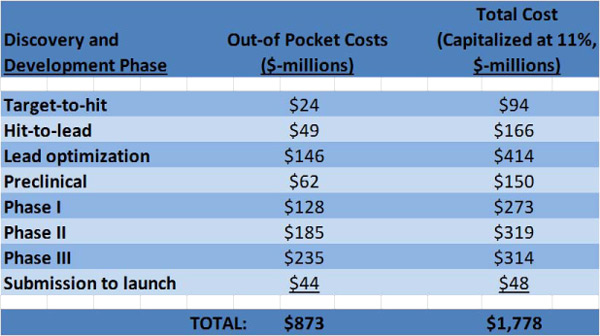

The magnitude of discovery and clinical costs up until the drug is launched are summarized in Figure 1.

Out-of-pocket costs are the actual cash outlays for the various phases in Figure 1. The cost of capital $905 million ($1,778 million – $873 million) is about equal to out-of-pocket costs. So, cost of capital is a big contributor to overall cost.

How does this relate to a small biotech company with only one drug in development? From the point of view of the CEO of that company, cost of capital is irrelevant, since the single goal of the company is to ferry the single drug candidate through clinical trials. Thus the CEO is interested only in whether enough money is available to complete clinical trials. Also, cost of failed drugs is irrelevant as there are no other drugs in the company’s pipeline. It is “do or die.” (Of course, for investors who expect to profit, the cost of their tied-up capital is very important. Venture capital investors want returns of 15% to 25% per year on their invested capital.)

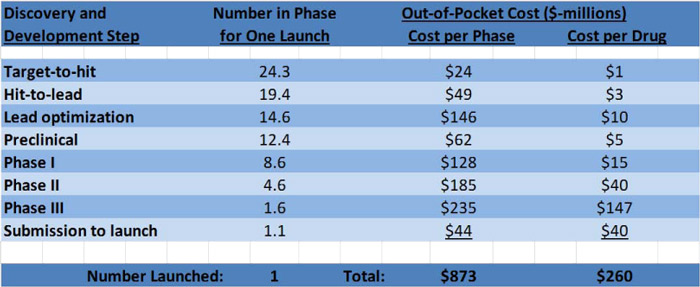

Let us also assume our small company is put together after successful preclinical trials and the cost through preclinical trials was covered by NIH grants. Figure 2 presents the data needed to calculate the real cost of drug development for our company.

Figure 1. Breakdown of discovery and development costs from the 2010 Eli Lilly study. The costs are discounted taking the year of FDA approval as the base year for discounting. Eleven percent is a typical interest rate used by the pharmaceutical industry to discount costs. The costs here are for both small molecule and biological new molecular entities (NMEs), defined as chemically unique pharmaceuticals that have not yet been marketed in the U.S. in any form.

For our company, only the money to cover out-of-pocket expenses for a single drug candidate (Figure 2, last column) for Phase I through launch is needed. This is $242 million. Still a significant amount of money, but nowhere near the $1.8 billion by big pharmaceutical company accounting.

The actual cost may be even lower. Since our company is small, perhaps a virtual company, it will employ a clinical research organization to conduct clinical trials. There are a number of such companies that are experts in conducting clinical trials, sometimes at less cost than the big pharmaceutical companies.

There is debate over whether costs are inflated as calculated by the methods used by Eli Lilly (Figures 1 and 2) and by the earlier DiMasi and colleagues papers. Light and Warburton, also respected economists, have challenged the methods leading to DiMasi’s cost findings. They claim that the DiMasi out-of-pocket cost estimates are much too high. Costs should be reduced by 50% because, in their words, “No adjustment was made for taxpayer subsidies or tax deductions and credits specifically tied to R&D expenditures.” They further argue that there are often very expensive outliers in drug discovery and development, so median costs not average costs should be used. The median cost turns out to be 74% of the average cost. Without taking sides in this debate, the point with regard to our company is that out-of-pocket drug development costs could be half of the $242 million calculated here, which is manageable for a promising drug with projected yearly sales of a few hundred million dollars.

In addition, Congress has smoothed the path to approval and guaranteed seven years exclusive marketing for orphan drugs for orphan diseases. The Orphan Drug Act was passed in 1983 to provide developers with benefits to encourage the discovery and development of drugs for rare diseases. Among the benefits are:

- Seven years of exclusive marketing regardless of patent status

- Tax incentives for clinical research

- Clinical trial design help from the FDA

- Clinical trial tax incentives

- Exemption from FDA filing fees

- Possible grant funding for Phase I and II clinical trials

A 2013 study by EvaluatePharma found that that Phase III clinical trial costs were $85 million for orphan drugs vs. $186 million for a nonorphan drugs.

The daunting $1.8 billion cost that might make someone give up before they begin has been reduced down to a manageable size.

Figure 2. Additional data from the 2010 Eli Lilly study. The second column lists the number of drug candidates at each phase, starting with 24.3 candidates and ending up with one FDA approved drug for launch into the marketplace. The last column is the middle column divided by the first column.

Lynn C. Klotz, Ph.D., is co-managing director of Bridging BioScience & BioBusiness. The material in this article comes from the Topic Books on Bridging BioScience & BioBusiness’ website.