March 1, 2011 (Vol. 31, No. 5)

Extensive Research Is Paying Off and Many New Therapeutic Approaches Are Being Pursued

There has been a fundamental shift in the immune system disorders market both in terms of the science behind the therapies and the way the sector has been generating revenues. Better understanding of the workings of the immune system has offered numerous biological targets for drug development leading to the emergence of novel therapeutic approaches. These developments are changing the entire landscape of the sector in multiple ways.

The availability of a potentially large patient pool makes this sector attractive for investors. However, how much of this optimism will be translated into dollars is uncertain since the sector is facing numerous technical, economic, and regulatory challenges. A recent report published by BCC Research predicts modest growth for the sector during the next five years. The report titled “Therapeutics for Immune System Disorders” estimates that the sector growth will be at a CAGR of 2.6 from $72 billion in 2010 to reach $82 billion by 2015.

Domination of TNF-Alpha Blockers

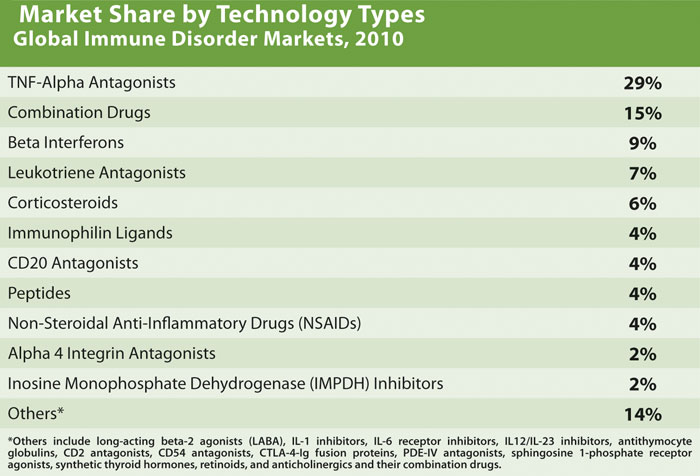

The BCC report quantifies the market share of biologics in immune disease treatments to be around 47% in 2010, which is expected to rise to 57% by 2015. TNF-alpha blockers dominated the market with 29% of the market share (Table). The safety and efficacy standards of these drugs have raised the bar very high for new drugs. The market failure of the IL-1 inhibitor Kineret from Amgen was mainly because it could not find a niche in the rheumatoid arthritis market.

Nevertheless, the recent success of Bristol-Myers Squibb’s Orencia offers new hopes for some of the non-TNF-alpha drugs, as more patients are being identified as nonrespondents to TNF-alpha blockers. Launched in 2005, Orencia could not gain market share in the midst of established TNF-alpha inhibitors. Recently, it found a niche in the treatment of nonrespondents to TNF-alpha blockers. The drug is on its way to becoming a blockbuster.

Changing Regulatory Landscape

Many governments are revisiting their healthcare policies by measuring the economic impact of high-priced drugs. Since some of these premium-priced drugs do not offer justifiable therapeutic benefits, additional recommendations are being sought with respect to each new therapy entering the market regarding their costs and benefits. While these are general concerns for the pharmaceutical industry as a whole, the impact will be significant in the immune disorders sector, which has almost 50% of its revenues generated from high-priced biologics.

Reimbursement groups including insurance companies and state reimbursement agencies are also applying pressure for reform of healthcare policies. Reference pricing, cost-benefit analysis, and health technology assessments are some of the mechanisms being employed to bring down the healthcare costs.

Immunosuppressant safety has always been a concern. A recent example of regulatory intervention is the safety controls announced by the U.S. FDA in February 2010 regarding the use of long-lasting beta agonists (LABA); the agency banned the use of LABAs as monotherapy to treat asthma and instituted new labeling requirements. The drugs that will be affected by this regulation include blockbuster drugs such as GlaxoSmithKline’s Advair and AstraZeneca’s Symbicort, both drugs contain corticosteroids and LABA.

In June 2010, FDA leveraged its power (based on a legislation passed in 2007) and ordered the companies to make labeling changes for these drugs. Similarly, FDA ordered inclusion of black-box warnings for several arthritis and autoimmune drugs such as Enbrel and Humira in September 2008 after these drugs were found to be associated with histoplasmosis—a potentially lethal fungal infection

Payor’s Market

Insurance companies promote generic drugs aggressively, and their policies significantly affect the sales of innovator brands after their patent expiry. Success of the combat strategies adopted by innovator companies such as introducing new, user-friendly formulations of the innovator brand rely largely on the cooperation of reimbursement agencies.

This is evident in the case of Prograf, a blockbuster immunosuppressant for transplant rejection. Generic tacrolimus products accounted for 44% of the market share in the United States in April 2010—soon after its patent expiry in late 2009. This rapid replacement was driven by the payment-withdrawal policy adopted by insurance companies that categorized Prograf as a Tier 4 drug, which made high co-payments from patients necessary. As a result of this policy that pushed the uptake of generics, the new once-daily formulation of tacrolimus (Advagraf) launched by Astellas to retain Prograf patients did not become successful in the U.S. market.

Even biologics are no longer free from competition, although the threat from biosimilars is lower due to the significant regulatory and technology challenges involved. However, bio-betters can become an emerging threat. These are the second-generation biologics that offer safer and more effective solutions such as the bio-better of Actemra under development by Femta Pharmaceuticals.

An IL-6 receptor inhibitor from Roche, Actemra is indicated for rheumatoid arthritis. The bio-better drug is expected to be more effective and convenient as it can be self-administered rather than injected. Investors have shown considerable interest in bio-betters since they offer less financial risk, as their clinical performance is already established—even though clinical trials are still required.

Clinical acceptance will ultimately decide the fate of these drugs. Since biologics are complicated therapies used to treat complex conditions, convincing physicians to switch to generic versions will be challenging. Moreover, prescribing generics is relatively unpopular in some countries such as France and Japan. Acceptance of biosimilars may prove to be even lower in those markets since additional worries over bioequivalence are involved. Hence, a push by payors to reduce expenditure may become a crucial factor that will decide the market share of innovator brands.

Traditionally, immune disease treatments have focused on controlling symptoms. Even though replacement-of-symptom treatments by targeted therapies is expected to follow the scientific breakthroughs of the sector, traditional methods still seem to be popular, at least in some immune disease segments. The market size of the symptom-treating drug market is expected to decline at a slow CAGR of -3% between 2010 and 2015.

Immune diseases are poorly understood, which makes symptom treatment all the more important. In addition, the multiple pathways involved in immune diseases complicate drug development efforts. Moreover, some diseases cannot be cured after onset. For example, once the pancreatic cells are destroyed by autoimmune reactions, type 1 diabetes patients have no alternative but to use insulin to survive. This is, in essence, treating the symptoms instead of regenerating the destroyed pancreatic cells.

Another important factor that helps to maintain demand for symptom-relief therapies is that some diseases already have effective, safe, and cheap remedies. For example, drugs such as histamine antagonists are effective and safe for controlling the annoying symptoms associated with seasonal allergies, which are not life-threatening conditions and normally get cured by themselves.

This sets the bar for new treatments high. The drugs that treat the underlying cause of allergies may result in unacceptable adverse reactions. Moreover, most of these drugs are now generic and affordable and it will be a challenge for developers to meet both the efficacy and cost advantages set by these drugs in the market. Hence, affordable and safe symptom-treatments are here to stay.

Syamala Ariyanchira, Ph.D. ([email protected]), is an associate with Singapore-based Polybus Consulting.